Usage Example

This page shows two complete, runnable examples using rule_significance_test() and plot_significance_test(). The first uses a strategy with a genuine signal so the test correctly finds significance. The second uses a strategy that fires entries at random so the test correctly finds no significance.

TIP

Make sure you have candles stored locally for the exchange, symbol, and timeframe you want to test. You can import them via the Jesse dashboard or the import_candles() research function.

Example 1 — Strategy with genuine edge (EMACrossover)

This strategy goes long when EMA 50 is above EMA 100 and ADX > 40, and short when the opposite is true. The ADX filter keeps it out of choppy, trendless markets. On BTC-USDT 4h from 2023-02-01 to 2024-07-01 the test finds a statistically significant signal.

TIP

For the purpose of rule significance testing, the strategy does not need to be complete. Only should_long() and should_short() matter — the signal collection phase never places orders, so go_long() and go_short() can simply pass.

Strategy file (strategies/EMACrossover/__init__.py):

from jesse.strategies import Strategy

import jesse.indicators as ta

class EMACrossover(Strategy):

def should_long(self) -> bool:

return ta.ema(self.candles, 50) > ta.ema(self.candles, 100) and ta.adx(self.candles) > 40

def should_short(self) -> bool:

return ta.ema(self.candles, 50) < ta.ema(self.candles, 100) and ta.adx(self.candles) > 40

def go_long(self):

pass

def go_short(self):

passTest script:

import logging

import os

import jesse.helpers as jh

from jesse.enums import exchanges

from jesse.research import get_candles, rule_significance_test, plot_significance_test

os.environ["RAY_DISABLE_IMPORT_WARNING"] = "1"

logging.getLogger("ray").setLevel(logging.ERROR)

# =============================================================================

# Configuration

# =============================================================================

EXCHANGE = exchanges.BINANCE_PERPETUAL_FUTURES

SYMBOL = "BTC-USDT"

TIMEFRAME = "4h"

START_DATE = "2023-02-01"

END_DATE = "2024-07-01"

WARM_UP_CANDLES = 210

config = {

"starting_balance": 10_000,

"fee": 0.0005,

"type": "futures",

"futures_leverage": 3,

"futures_leverage_mode": "cross",

"exchange": EXCHANGE,

"warm_up_candles": WARM_UP_CANDLES,

}

routes = [

{

"exchange": EXCHANGE,

"strategy": "EMACrossover",

"symbol": SYMBOL,

"timeframe": TIMEFRAME,

}

]

# =============================================================================

# Fetch candles

# =============================================================================

warmup_candles, trading_candles = get_candles(

EXCHANGE,

SYMBOL,

TIMEFRAME,

jh.date_to_timestamp(START_DATE),

jh.date_to_timestamp(END_DATE),

WARM_UP_CANDLES,

caching=True,

is_for_jesse=True,

)

candles = {

jh.key(EXCHANGE, SYMBOL): {

"exchange": EXCHANGE,

"symbol": SYMBOL,

"candles": trading_candles,

}

}

warmup = {

jh.key(EXCHANGE, SYMBOL): {

"exchange": EXCHANGE,

"symbol": SYMBOL,

"candles": warmup_candles,

}

}

# =============================================================================

# Run the test

# =============================================================================

result = rule_significance_test(

config = config,

routes = routes,

data_routes = [],

candles = candles,

warmup_candles = warmup,

n_simulations = 1000,

random_seed = 42,

progress_bar = True,

)

# =============================================================================

# Print results

# =============================================================================

p = result["p_value"]

if p <= 0.001:

label = "HIGHLY SIGNIFICANT (p ≤ 0.001) ★★★"

elif p <= 0.01:

label = "VERY SIGNIFICANT (p ≤ 0.01) ★★"

elif p <= 0.05:

label = "STATISTICALLY SIGNIFICANT (p ≤ 0.05) ★"

elif p <= 0.10:

label = "POSSIBLY SIGNIFICANT (p ≤ 0.10) ~"

else:

label = "not significant (p > 0.10)"

print(f"\n{'='*60}")

print(f" Rule Significance Test — Bootstrap")

print(f"{'='*60}")

print(f" Observations : {result['n_observations']} bars")

print(f" Simulations : {result['n_simulations']}")

print(f" Observed mean : {result['observed_mean']:.8f}")

print(f" Annualised return : {result['annualized_return'] * 100:.4f} %")

print(f" p-value : {p:.4f} → {label}")

print(f"{'='*60}\n")

plot_significance_test(result)Output:

============================================================

Rule Significance Test — Bootstrap

============================================================

Observations : 3095 bars

Simulations : 1000

Observed mean : 0.00014333

Annualised return : 3.6120 %

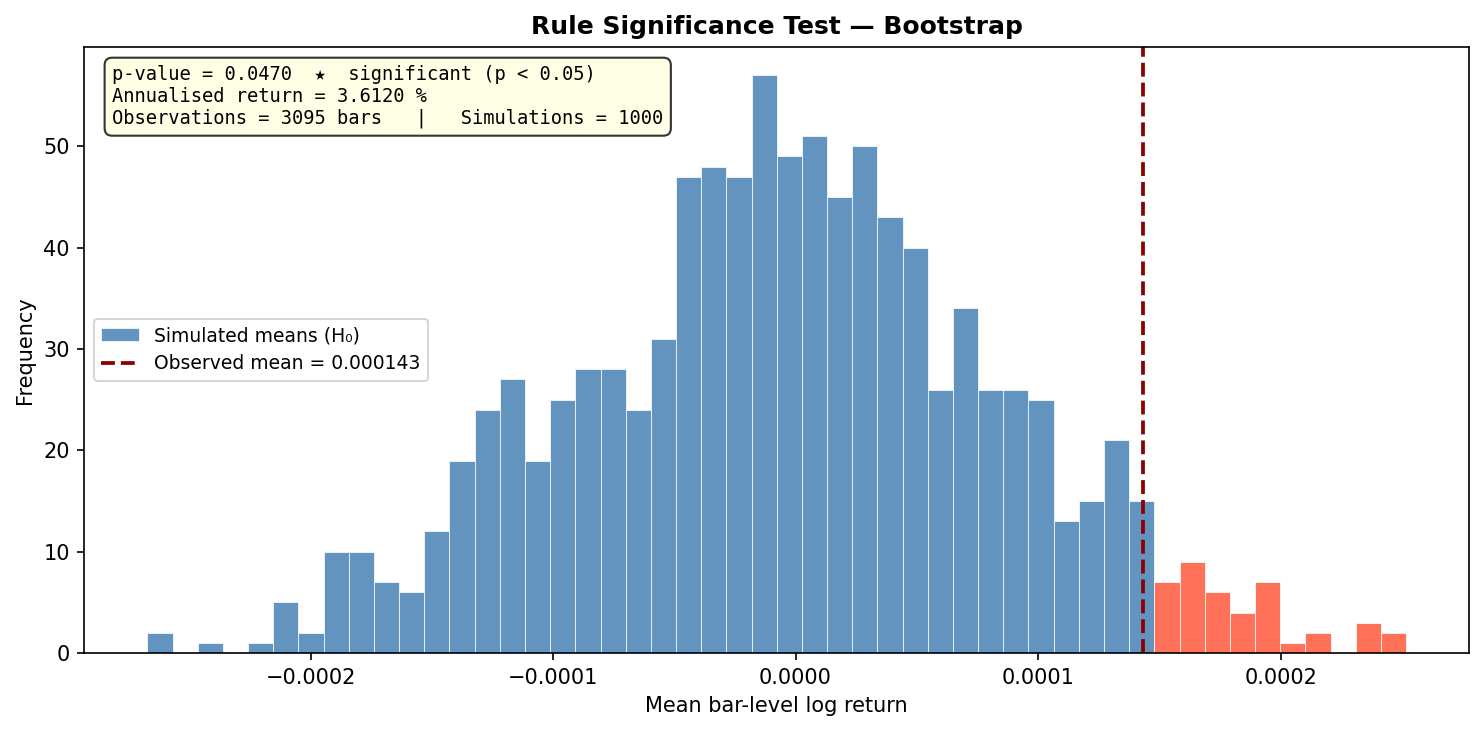

p-value : 0.0470 → STATISTICALLY SIGNIFICANT (p ≤ 0.05) ★

============================================================The p-value of 0.047 means only 4.7 % of random bootstrap resamples matched or beat the rule's observed mean. The ADX filter gives the crossover a genuine edge on this period.

Example 2 — Strategy with no edge (RandomSignal)

This strategy fires long 80 % of the time, short 5 %, and stays flat 15 % — all chosen at random with no regard for market conditions. The null hypothesis should not be rejected and the p-value should be well above 0.05.

Strategy file (strategies/RandomSignal/__init__.py):

import random

from jesse.strategies import Strategy

class RandomSignal(Strategy):

def should_long(self) -> bool:

return random.Random(42 + self.index).random() < 0.80

def should_short(self) -> bool:

r = random.Random(42 + self.index).random()

return 0.80 <= r < 0.85

def go_long(self):

pass

def go_short(self):

passThe RNG is seeded from self.index so the same bar always produces the same signal, making results reproducible across repeated runs.

Test script:

import logging

import os

import jesse.helpers as jh

from jesse.enums import exchanges

from jesse.research import get_candles, rule_significance_test, plot_significance_test

os.environ["RAY_DISABLE_IMPORT_WARNING"] = "1"

logging.getLogger("ray").setLevel(logging.ERROR)

# =============================================================================

# Configuration

# =============================================================================

EXCHANGE = exchanges.BINANCE_PERPETUAL_FUTURES

SYMBOL = "BTC-USDT"

TIMEFRAME = "4h"

START_DATE = "2023-02-01"

END_DATE = "2024-07-01"

WARM_UP_CANDLES = 210

config = {

"starting_balance": 10_000,

"fee": 0.0005,

"type": "futures",

"futures_leverage": 3,

"futures_leverage_mode": "cross",

"exchange": EXCHANGE,

"warm_up_candles": WARM_UP_CANDLES,

}

routes = [

{

"exchange": EXCHANGE,

"strategy": "RandomSignal",

"symbol": SYMBOL,

"timeframe": TIMEFRAME,

}

]

# =============================================================================

# Fetch candles

# =============================================================================

warmup_candles, trading_candles = get_candles(

EXCHANGE,

SYMBOL,

TIMEFRAME,

jh.date_to_timestamp(START_DATE),

jh.date_to_timestamp(END_DATE),

WARM_UP_CANDLES,

caching=True,

is_for_jesse=True,

)

candles = {

jh.key(EXCHANGE, SYMBOL): {

"exchange": EXCHANGE,

"symbol": SYMBOL,

"candles": trading_candles,

}

}

warmup = {

jh.key(EXCHANGE, SYMBOL): {

"exchange": EXCHANGE,

"symbol": SYMBOL,

"candles": warmup_candles,

}

}

# =============================================================================

# Run the test

# =============================================================================

result = rule_significance_test(

config = config,

routes = routes,

data_routes = [],

candles = candles,

warmup_candles = warmup,

n_simulations = 1000,

random_seed = 42,

progress_bar = True,

)

# =============================================================================

# Print results

# =============================================================================

p = result["p_value"]

if p <= 0.001:

label = "HIGHLY SIGNIFICANT (p ≤ 0.001) ★★★"

elif p <= 0.01:

label = "VERY SIGNIFICANT (p ≤ 0.01) ★★"

elif p <= 0.05:

label = "STATISTICALLY SIGNIFICANT (p ≤ 0.05) ★"

elif p <= 0.10:

label = "POSSIBLY SIGNIFICANT (p ≤ 0.10) ~"

else:

label = "not significant (p > 0.10)"

print(f"\n{'='*60}")

print(f" Rule Significance Test — Bootstrap")

print(f"{'='*60}")

print(f" Observations : {result['n_observations']} bars")

print(f" Simulations : {result['n_simulations']}")

print(f" Observed mean : {result['observed_mean']:.8f}")

print(f" Annualised return : {result['annualized_return'] * 100:.4f} %")

print(f" p-value : {p:.4f} → {label}")

print(f"{'='*60}\n")

plot_significance_test(result)Output:

============================================================

Rule Significance Test — Bootstrap

============================================================

Observations : 3095 bars

Simulations : 1000

Observed mean : 0.00020504

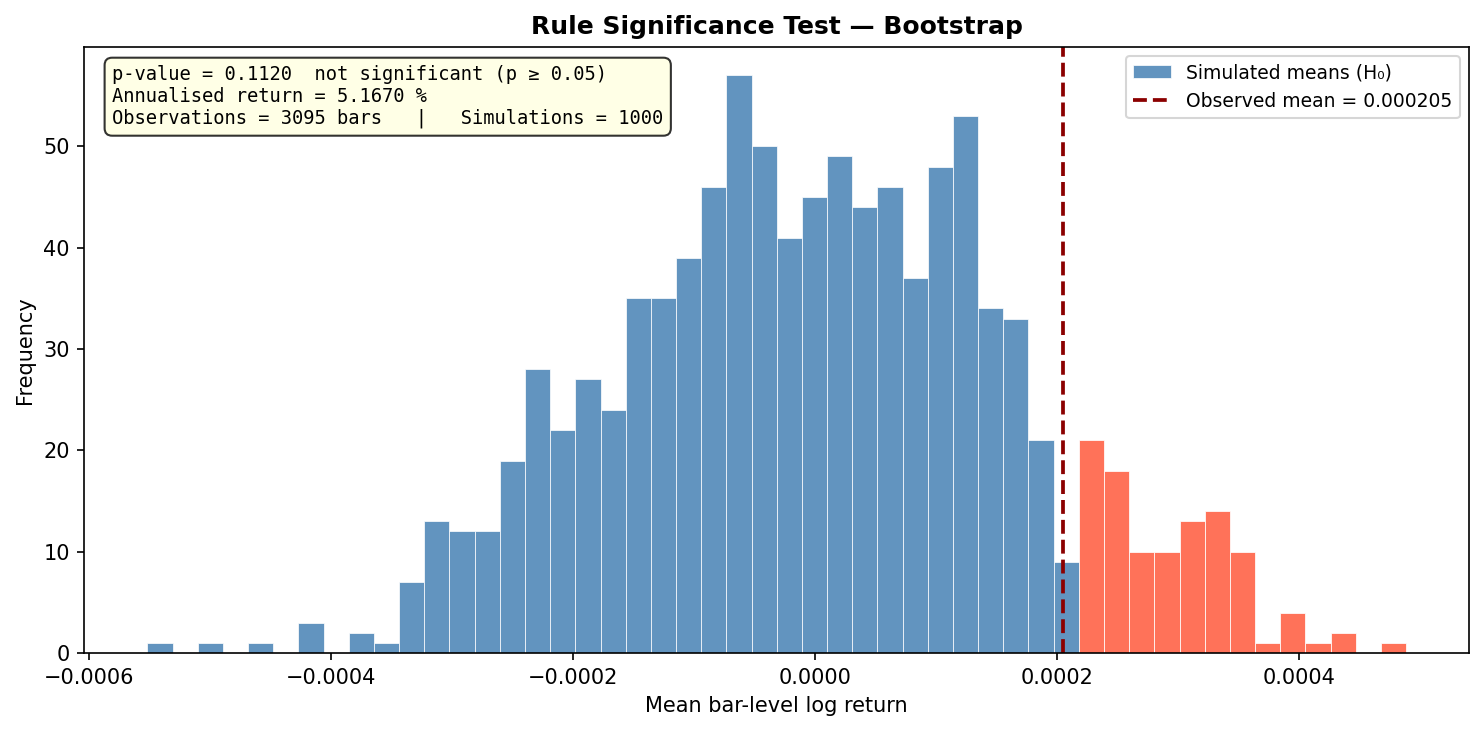

Annualised return : 5.1670 %

p-value : 0.1120 → not significant (p > 0.10)

============================================================Despite a positive observed mean (BTC trended up during this period, so even random longs captured some drift), the p-value of 0.112 confirms there is no genuine signal — 11.2 % of random resamples matched or beat it, which is well within the range of chance.

Parameters reference

- config (dict): Strategy configuration — same format as

research.backtest(). Must includestarting_balance,fee,type,futures_leverage,futures_leverage_mode,exchange, andwarm_up_candles. - routes (list): Exactly one trading route. The strategy must implement

should_long()and/orshould_short()to emit meaningful signals. - data_routes (list): Any number of data-only routes that the strategy reads via

self.get_candles()but does not trade on. - candles (dict): Candles for the trading period, keyed by

jh.key(exchange, symbol). - warmup_candles (dict, optional): Warm-up candles in the same key format. Pass the array returned by

get_candles(..., is_for_jesse=True). - hyperparameters (dict, optional): Hyperparameter overrides forwarded to the strategy's

hyperparameters()method. - n_simulations (int, default=

200): Number of bootstrap resamples. At least1000is recommended for a reliable p-value. - random_seed (int, optional): Base random seed for reproducibility.

- progress_bar (bool, default=

False): Show atqdmprogress bar during the simulation phase. - cpu_cores (int, optional): Number of parallel Ray workers. Defaults to 80 % of available cores.

Return value

rule_significance_test() returns a dict with the following keys:

- observed_mean (float): Mean bar-level log return of the rule after detrending.

- annualized_return (float):

observed_mean × 252— a rough annualised estimate. - simulated_means (np.ndarray): Shape

(n_simulations,). The full bootstrap null distribution. - p_value (float): Fraction of simulated means ≥

observed_mean. At or below0.10is possibly significant; at or below0.05is statistically significant; at or below0.001is highly significant. - n_simulations (int): Number of simulations completed.

- n_observations (int): Number of bars used after warmup and NaN removal.

See Interpreting Results for a full guide on reading these numbers.